![What Is Monetary Literacy? Instruments to Succeed [+ Free Templates]](https://i0.wp.com/www.chime.com/wp-content/uploads/2019/04/at-the-reading-corner-of-papersun-apartment-taiwan_t20_yRzYP6.jpg?fit=%2C&ssl=1 "What Is Monetary Literacy? Instruments to Succeed [+ Free Templates]")

[ad_1]

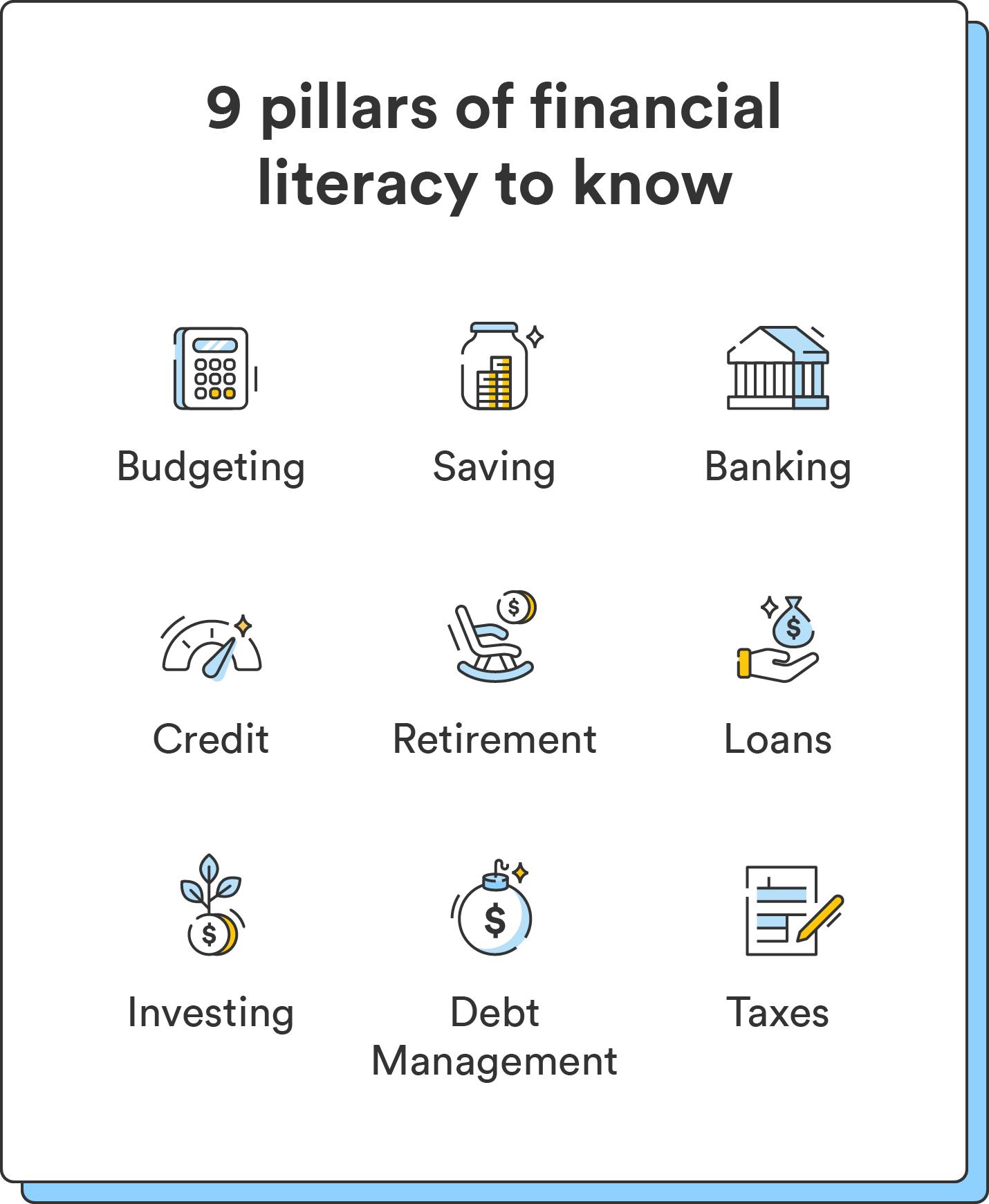

Monetary literacy encompasses many various subjects. Budgeting, saving, investing, and debt administration every play a significant function in your monetary well-being. Check out the core pillars of economic literacy under.

Budgeting

Budgeting is a cornerstone of economic wellness and entails managing your month-to-month earnings and bills to align together with your means and monetary targets. Efficient budgeting helps you keep away from or repay debt, pay your payments on time, put together for upcoming bills, and be certain that you meet your short- and long-term wants.

There are numerous methods to funds, like:

The strategy you select doesn’t matter so long as it really works for you. A stable funds will embody a mounted and variable bills listing, your month-to-month earnings, short-term and long-term financial savings targets, and future bills.

53% of these with larger monetary literacy reported that they spend lower than their earnings, in comparison with solely 35% of these with decrease monetary literacy.8

Saving

Saving is a vital a part of monetary literacy that means that you can construct a security internet for sudden bills, obtain your targets, and put together for the longer term. It entails setting apart a portion of your earnings for the longer term for issues like:

- Emergencies

- Main purchases

- Lengthy-term investments

If you happen to don’t recurrently save, an sudden expense can turn into a a lot bigger setback. Say your automotive breaks down, and also you want $1,500 to repair it. You don’t have any cash saved to cowl it, however you want your automotive to get to work – so you’re taking out a high-interest mortgage or money advance to cowl the price. Whereas this solves the issue within the brief time period, you’re now on the hook for paying again that mortgage with added curiosity, costing you extra in the long term.

50% of adults aged 18 to 29 haven’t saved an emergency fund that covers three months of bills.²

Constructing a behavior of recurrently saving offers peace of thoughts and monetary stability and opens the door to reaching your financial savings targets. That may very well be paying for an house deposit or a mortgage to your first residence, aircraft tickets for a visit, or anything you need to save for. Saving is a device that may unlock alternatives, goals, and targets to your future.

If you happen to’re questioning how a lot to save lots of every month, begin with 20% of every paycheck. You can even automate your financial savings by establishing an computerized switch out of your checking account to your financial savings account.

Banking

One other pillar of economic literacy is banking and financial institution accounts. You’ll want a checking account for every part from utilizing a debit card, bank card, or ATM to making use of for a house mortgage. They provide comfort and a protected option to retailer your funds. Listed here are some widespread varieties of financial institution accounts:

Begin by selecting a checking account with a monetary establishment that meets your wants and targets. You’ll need to evaluate totally different banks or credit score unions primarily based on charges, rates of interest, and ease of use. A checking account additionally means that you can use instruments like direct deposit, which deposits your paycheck straight into your account every month.

You’ll additionally need to determine on a financial savings account to retailer your financial savings. Whereas checking accounts are used for day-to-day transactions, financial savings accounts are separate locations to retailer funds you don’t contact typically. They permit you to earn curiosity to develop your cash for upcoming purchases. When selecting a financial savings account, evaluate every account’s charges, phrases, rates of interest, and withdrawal limits.

You may obtain our checking account data printable to maintain your account particulars in a single place.

4.5% of U.S. households are unbanked and don’t have a checking account at an insured monetary establishment.9

Credit score

Credit score refers to your borrowing historical past and the way nicely you handle credit score and debt. Your credit score impacts your skill to be permitted for loans, bank cards, and different monetary merchandise and safe favorable rates of interest. A credit score rating can be mandatory for monetary merchandise, like automotive loans or mortgages.

Once you open any sort of credit score account, your credit score historical past is analyzed by credit score bureaus primarily based on 5 components:

- Fee historical past (35%)

- Credit score utilization (30%)

- Size of credit score historical past (15%)

- Functions for brand new credit score (10%)

- Kinds of credit score used (10%)

Based mostly in your account exercise, you’re given a credit score rating related together with your credit score report. That impacts whether or not you qualify for a mortgage or safe decrease rates of interest.

To determine credit score, you can begin by opening a bank card or acquiring a small mortgage and making constant, on-time funds. Paying on time might help you develop a historical past of accountable credit score utilization and construct up your credit score rating step by step. If you happen to’ve by no means had credit score earlier than or have a poor rating, it’s possible you’ll want to begin with a secured bank card.

Whereas there are various benefits to utilizing credit score, bear in mind the influence of poor credit score habits in your funds. Not paying your payments on time, maxing out your card, and spending greater than you possibly can afford can go away you with excessive quantities of debt and costly curiosity prices that add up quick.

The common bank card holder has $5,474 in debt.10

Debt administration

Debt represents cash you owe to a lender, who prices you an rate of interest to borrow the funds. You’ll doubtless have to take out some type of debt in your life, whether or not it’s pupil loans for school, a house mortgage, or utilizing a bank card for a big buy. Several types of debt have totally different advantages and penalties:

- Mortgages and residential loans enable for homeownership however carry the chance of foreclosures for those who miss funds.

- Scholar loans present a path to larger schooling however can even result in excessive ranges of pupil debt with out a clear compensation plan.

- Bank cards provide comfort and suppleness however can result in high-interest debt burdens if not managed responsibly.

To borrow cash responsibly, ask your self whether or not you possibly can afford the debt and assessment the phrases, together with rates of interest, compensation phrases, and some other charges. If money owed are left unpaid, you’ll accrue curiosity prices on high of the stability you owe, costing you way more in the long term.

Once you perceive the dangers and obligations of borrowing cash, you possibly can keep away from unneeded monetary stress, keep away from feeling trapped in debt, and use sure varieties of debt to your benefit (like constructing your credit score rating).

18% of U.S. customers mentioned their essential supply of debt is their residence mortgage, and 20% mentioned their essential supply of debt is bank card debt. 11

Loans

Loans can present a option to finance main bills, like shopping for a automotive or pursuing faculty, with out a big upfront fee. Additionally they present a structured compensation plan so you possibly can funds successfully to make sure the mortgage will get paid off. Understanding loans and their influence in your funds might help you make knowledgeable monetary choices.

There are several types of loans, like:

There are additionally prices related to getting a mortgage, and also you’ll need to consider totally different mortgage choices primarily based in your wants. Researching and evaluating loans from totally different lenders might help you discover probably the most favorable phrases, charges, and compensation plans.

Whereas loans can present entry to giant bills, they’re a debt that usually requires curiosity funds. Paying extra in curiosity will increase your general value of borrowing, so perceive how a lot you’ll pay in curiosity over a mortgage time period to make a sound determination.

Take into account the long-term implications of taking out a mortgage and the way a lot it should value you over time. Evaluating whether or not a mortgage aligns together with your targets and is inside your means will assist you to be a financially literate borrower.

Gen X has a median pupil mortgage debt of roughly $45,800, the very best throughout all generations. Gen Z has a median whole pupil mortgage debt of $20,470.12

Investing

Investing helps you maximize your monetary potential and discover alternatives to develop your wealth. Investing means shopping for securities like shares, bonds, mutual funds, ETFs, and different investments that develop in worth over time. And the earlier you begin investing, the extra time your cash has to develop.

A part of understanding this pillar of economic literacy is realizing how to decide on the best investments. This is determined by a number of components:

- Your age and time horizon (how a lot time you need to hold your funds invested)

- Your threat tolerance

- Your short- and long-term monetary targets

One key to deciding what to put money into is the idea of threat and return. All investments carry some threat, and a few are much less dangerous than others. These nearer to retirement are doubtless to decide on much less dangerous investments, whereas those that are a long time away might go for riskier investments with the potential for larger returns.

You may mitigate threat by means of one other key investing precept: diversification. Diversification means spreading your investments throughout numerous asset courses and sectors to scale back your general threat. Diversification helps defend your funding portfolio from market volatility and the poor efficiency of any single funding.

Your age, earnings, and monetary targets will decide your finest funding selections. You don’t want some huge cash to begin investing, and also you don’t have to be an professional to construct a stable portfolio. On-line brokerages or robo-advisors are a preferred option to begin investing that doesn’t require an costly monetary advisor. Many will assist you to make funding choices primarily based in your targets and threat tolerance.

Over two thirds of newbie buyers really feel like they want extra assets to make funding choices that influence their future.13

Retirement

Retirement planning entails setting your self up financially to your retirement years. When you grasp different elements of economic literacy, like budgeting and saving, constructing credit score, and managing debt, you can begin fascinated by methods to construct your wealth for retirement.

62% of 18 to 29-year-old adults haven’t any retirement financial savings.14

Understanding your funds might help you begin fascinated by how a lot cash it’s possible you’ll have to retire comfortably. Take into account the varieties of bills you’ll have down the road and the way a lot cash you’ll have to afford them. You don’t have to know precisely how a lot cash you’ll want to begin saving and planning. What issues is that you just take steps towards rising your financial savings particularly to your retirement years.

There are several types of retirement accounts and financial savings automobiles that may maximize your retirement financial savings, like:

These include totally different tax advantages, phrases, and contribution limits, and also you’ll want to think about which possibility finest aligns together with your distinctive targets and circumstances.

Considering by means of your retirement targets, envisioning the life-style you propose to guide, and making a plan to make sure monetary safety in your later years are all essential elements of economic literacy – and the earlier you begin, the extra time you need to save. Undecided the place to begin? Our retirement planning printable might help you navigate essential motion gadgets:

33% of People count on to must hold working after they retire to keep up a snug lifestyle.15

Taxes

Monetary literacy relating to taxes covers realizing how taxes can influence your earnings and funds. There are several types of taxes, akin to:

- Revenue tax

- Gross sales tax

- Property tax

- Capital good points tax

Every has its personal guidelines and implications, and being conscious of the totally different charges, deductions, and credit might help you reduce your tax legal responsibility.

Staying organized and protecting correct data can be essential for tax administration. To file your taxes correctly, hold observe of your earnings, bills, and related paperwork like receipts and monetary statements. Realizing easy methods to declare deductions and credit can even assist you to make extra knowledgeable choices when submitting your taxes.

Taxes are advanced, and it’s possible you’ll ultimately take into account working with a monetary advisor to make sure you perceive totally different tax legal guidelines and the way they apply to your distinctive scenario. Proactively planning and assembly tax obligations might help you maximize your tax advantages.

40% of U.S. households fail to pay their earnings taxes.16